How I Tamed My Mortgage and Started Building Wealth — A Beginner’s Journey with Real Investment Tools

Buying my first home felt like winning the lottery—until I saw the monthly mortgage number. I was overwhelmed, confused, and honestly a little scared. But over time, I discovered simple, practical investment tools that didn’t just help me manage my debt but actually turned my home into a stepping stone for financial growth. This is how I went from stress to strategy, one smart move at a time. The journey wasn’t about sudden windfalls or risky bets. It was about making steady, informed choices that aligned my mortgage with long-term wealth. For many, a home is the largest financial commitment they’ll ever make. But with the right mindset and tools, it can also become the foundation of financial freedom.

The Mortgage Moment: When Reality Hits

Purchasing a home is often celebrated as a major life achievement, a symbol of stability and success. Yet for many first-time buyers, the excitement quickly gives way to a sobering reality—the weight of a mortgage. The initial joy of holding the keys can fade when the monthly payment arrives, especially when it consumes a large portion of income. This moment of realization is common and powerful. It’s not just about budgeting; it’s about confronting the long-term financial responsibility that comes with homeownership.

For years, I viewed my mortgage solely as a debt—a necessary evil that had to be paid. I focused only on making the minimum payments, believing that any extra money should go toward reducing the principal as quickly as possible. This mindset, while understandable, limited my financial potential. I wasn’t thinking about how my home could do more than just provide shelter. I wasn’t considering it as an asset that could be part of a broader financial strategy. The shift began when I started to see my home not just as a cost, but as a foundational piece of my financial life.

This change in perspective didn’t happen overnight. It came from learning how wealth is built—not just through saving, but through strategic use of assets. A home, unlike a car or a vacation, typically appreciates in value over time. While it requires ongoing expenses, it also has the potential to grow in worth and generate equity. When managed wisely, a mortgage doesn’t have to be a burden. It can be a tool that, when combined with smart investing, helps build long-term wealth. The key is to stop seeing the mortgage in isolation and start integrating it into a larger financial plan.

Early decisions matter. How you structure your payments, whether you automate savings, and how you handle extra income can all influence your financial trajectory. Many people wait years before realizing they could have been building wealth alongside paying down debt. Starting early—even with small steps—can make a significant difference. The emotional relief of paying off debt is real, but the financial reward of investing wisely over time can be even greater. The goal isn’t to ignore the mortgage, but to manage it in a way that supports both security and growth.

Investment Tools Beyond the Basics: What Beginners Overlook

Most new homeowners focus almost exclusively on their mortgage payments, often overlooking the opportunity to grow wealth through parallel investment strategies. The instinct to prioritize debt repayment is natural, especially when the numbers feel overwhelming. However, this single-minded focus can cause people to miss out on powerful tools that are accessible, low-risk, and designed to grow money steadily over time. The truth is, managing a mortgage doesn’t have to mean putting all financial energy into repayment. There are practical investment options that can work alongside a mortgage, even on a modest income.

One of the most effective tools is the high-yield savings account. Unlike traditional savings accounts that offer minimal interest, high-yield versions—often provided by online banks—deliver significantly better returns with little to no added risk. These accounts are FDIC-insured, meaning your money is protected up to federal limits. By placing emergency funds or short-term savings in such accounts, homeowners can earn passive income while maintaining liquidity. Over time, the compounding effect can add up, especially when contributions are consistent.

Another essential tool is the tax-advantaged retirement account, such as a 401(k) or IRA. Many employers offer matching contributions for 401(k) plans, which is essentially free money. Even if you’re making minimum mortgage payments, contributing enough to get the full employer match is a smart move. The tax benefits alone—whether through tax-deferred growth in a traditional IRA or tax-free withdrawals in a Roth IRA—can significantly boost long-term savings. These accounts are designed to grow wealth over decades, and starting early maximizes the power of compounding.

Low-cost index funds are another cornerstone of beginner-friendly investing. These funds track broad market indices like the S&P 500 and offer instant diversification. Because they are passively managed, they come with lower fees than actively managed funds, which means more of your money stays invested. Historically, the stock market has delivered average annual returns of about 7% to 10% over the long term, after inflation. While past performance doesn’t guarantee future results, the data shows that consistent investment in index funds can outpace the interest costs of a typical mortgage over time.

The key is consistency, not size. You don’t need large sums to benefit from these tools. Even setting aside $50 or $100 a month can make a meaningful difference when done regularly. The goal is to build a habit of investing, just as you’ve built the habit of making mortgage payments. Over time, these small contributions grow, creating a parallel path to financial security. By using these accessible tools, homeowners can move beyond the cycle of debt and begin actively building wealth.

Pay Off Debt or Invest? The Balancing Act

One of the most common financial dilemmas for new homeowners is deciding whether to allocate extra funds toward paying off the mortgage faster or investing them elsewhere. This decision often feels emotional as much as financial. On one side is the powerful appeal of debt freedom—the peace of mind that comes from knowing you owe less and have more control over your home. On the other side is the long-term potential of investing, where money has the chance to grow at a rate that could exceed the cost of the mortgage. There’s no single right answer, but understanding the trade-offs can help make a more informed choice.

From a mathematical standpoint, the decision often comes down to interest rates. Most fixed-rate mortgages carry interest rates between 3% and 6%, depending on market conditions and creditworthiness. Meanwhile, historical stock market returns—again, through broad index funds—have averaged around 7% to 10% annually over long periods. This suggests that, on average, investing may offer higher returns than the interest saved by paying down a mortgage early. For example, if your mortgage rate is 5%, and you expect a 7% return from investing, you’re likely better off investing the extra cash, assuming you’re comfortable with market fluctuations.

However, numbers don’t tell the whole story. Risk tolerance plays a crucial role. Investing involves volatility—there will be years when returns are negative. For some people, the stress of market swings outweighs the potential gains. In contrast, making extra mortgage payments provides a guaranteed return equal to the interest rate, with no risk. This certainty can be emotionally valuable, especially for those who prioritize stability over growth.

The best approach often lies in balance. Some financial experts recommend a hybrid strategy: making minimum mortgage payments while also investing a portion of extra income. This allows homeowners to benefit from both debt reduction and market growth. Another option is to set specific milestones—such as building a six-month emergency fund or paying off high-interest credit card debt—before increasing investment contributions. The goal is to create a plan that aligns with personal values, risk tolerance, and long-term goals.

It’s also important to consider tax implications. Mortgage interest may be tax-deductible in some cases, which can lower the effective interest rate. Meanwhile, investment gains may be subject to capital gains taxes, though long-term holdings often benefit from lower rates. These factors don’t change the decision dramatically for most people, but they add nuance to the overall picture. Ultimately, the choice between paying off debt and investing isn’t about perfection—it’s about progress. What matters most is taking action, staying consistent, and adjusting the strategy as life changes.

Automating Financial Growth: Systems That Work Without Willpower

Maintaining financial discipline over years or decades is challenging, especially when life gets busy. Relying on motivation alone—waiting to feel inspired to save or invest—is rarely enough. The real secret to long-term success lies in building systems that work automatically, removing the need for constant decision-making. Automation is one of the most powerful tools available to homeowners who want to grow wealth without added stress. By setting up automatic transfers, investment contributions, and payment schedules, you create a financial structure that supports your goals whether you’re thinking about them or not.

The foundation of this system is direct deposit allocation. As soon as your paycheck arrives, a portion can be directed automatically into savings, retirement accounts, or investment platforms. Many employers allow you to split your direct deposit across multiple accounts, making it easy to fund both short-term needs and long-term goals. For example, you might send 70% of your paycheck to your checking account, 20% to a high-yield savings account, and 10% to a Roth IRA. This ensures that saving and investing happen first, before you have a chance to spend the money.

Investment platforms also offer automation features. Services like robo-advisors allow you to set up recurring investments in low-cost index funds based on your risk profile. You can schedule weekly, biweekly, or monthly contributions that align with your pay cycle. Over time, these small, consistent investments build momentum through dollar-cost averaging—buying more shares when prices are low and fewer when prices are high, which reduces overall risk.

Another useful tool is round-up apps, which link to your debit or credit card and automatically invest the spare change from everyday purchases. For instance, if you buy coffee for $3.75, the app rounds up to $4.00 and invests the $0.25 difference. While each amount is small, the cumulative effect can be significant over months and years. These apps make investing feel effortless and almost invisible, which helps people stay consistent without feeling deprived.

The power of automation isn’t just in convenience—it’s in consistency. Financial growth rarely comes from dramatic actions, but from small, repeated behaviors. By removing the need for willpower, automation ensures that progress continues even during busy or stressful times. It transforms financial goals from aspirations into habits. For homeowners managing a mortgage, this kind of system provides peace of mind, knowing that wealth is being built steadily in the background, alongside monthly payments.

Refinancing as a Strategic Move, Not Just a Rate Chase

Refinancing a mortgage is often viewed as a way to lower monthly payments, but it can be much more than that when approached strategically. Done wisely, refinancing can free up cash flow, reduce total interest paid, and even create opportunities to redirect funds toward investment. However, it’s not a decision to be made lightly. There are costs involved, including closing fees, and extending the loan term can sometimes result in paying more over time, even with a lower rate. The key is to treat refinancing not as a reflex, but as a calculated financial move aligned with long-term goals.

One of the most effective uses of refinancing is to shorten the loan term while maintaining affordability. For example, switching from a 30-year mortgage to a 15-year loan can significantly reduce the total interest paid over the life of the loan. Even if the monthly payment increases slightly, the long-term savings can be substantial. This approach works well for homeowners whose income has increased or whose financial situation has stabilized. It allows them to build equity faster while still keeping payments manageable.

Another strategic reason to refinance is to access home equity for investment purposes. Some homeowners use cash-out refinancing to fund home improvements that increase property value or to invest in diversified portfolios. While this carries risk—since you’re borrowing against your home—it can make sense if the expected return on investment exceeds the mortgage rate. For instance, if you refinance at 4% and invest in a low-cost index fund with a historical return of 7%, the math may support the decision. However, this should only be done with careful planning and a clear understanding of the risks.

Timing matters. The break-even point—the time it takes for monthly savings to offset closing costs—is a critical factor. If you plan to stay in the home for several years, refinancing can be worthwhile. But if you expect to move soon, the costs may outweigh the benefits. It’s also important to monitor interest rate trends. Refinancing when rates are significantly lower than your current rate can lead to meaningful savings, but chasing every small drop isn’t necessary. A general rule of thumb is to consider refinancing if the new rate is at least 0.5% to 1% lower than your current rate.

Finally, refinancing should be part of a broader financial strategy, not a standalone action. It’s not just about reducing payments—it’s about creating room in the budget to invest, save, or reduce other debts. When used with intention, refinancing can be a powerful tool for accelerating financial progress. The goal is to make the mortgage work for you, not just to reduce a number on a bill.

Tracking Progress: Measuring What Really Matters

Without clear feedback, it’s easy to feel stuck or discouraged, even when you’re making progress. Many homeowners focus only on their mortgage balance, celebrating each dollar paid down but missing the bigger picture of their overall financial health. To build true wealth, it’s essential to track meaningful metrics that reflect growth, not just debt reduction. The right measurements can provide motivation, reveal trends, and guide better decisions over time.

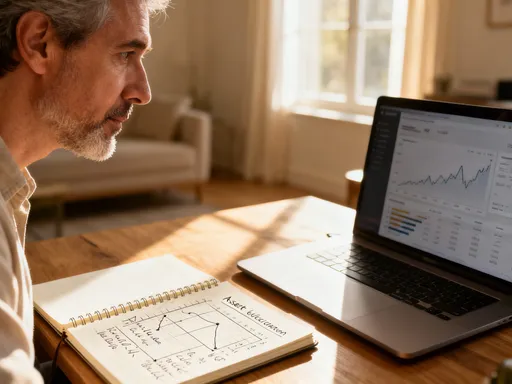

One of the most powerful indicators is net worth—the difference between what you own and what you owe. This includes your home’s current market value, investment accounts, savings, and other assets, minus debts like the mortgage, car loans, and credit card balances. Tracking net worth monthly or annually shows whether your financial position is improving, regardless of individual account fluctuations. Even if your mortgage balance changes slowly, growth in investment accounts or home equity can drive net worth upward, providing a more accurate picture of progress.

Another key metric is investment account momentum. Are your balances growing consistently? Are contributions increasing over time? Monitoring the rate of growth in retirement and brokerage accounts helps assess whether your investment strategy is working. Visual tools like charts or graphs can make this progress more tangible, turning abstract numbers into a clear story of forward movement. Many financial platforms offer built-in dashboards that track performance over time, making it easier to stay informed.

The debt-to-asset ratio is another useful measure. This compares your total debt to your total assets and gives a sense of financial leverage. As you pay down debt and grow assets, this ratio should improve, indicating greater financial stability. A lower ratio often means better borrowing power and more flexibility in financial decisions. It’s not about eliminating all debt—some debt, like a mortgage, can be productive—but about maintaining a healthy balance.

Annual financial reviews are an excellent way to consolidate this data. Set aside time each year to assess your budget, update your net worth, review investment performance, and adjust goals. This practice helps you stay aligned with your long-term vision and make informed adjustments. Tracking progress isn’t about perfection—it’s about awareness. When you can see how your actions translate into real results, it becomes easier to stay committed and make smarter choices.

Building Confidence Through Small Wins

Financial transformation doesn’t happen in a single moment. It’s the result of small, consistent actions that build over time. For many homeowners, the journey begins with fear—fear of debt, fear of making mistakes, fear of not doing enough. But confidence grows not from perfection, but from action. Each small win—making the first investment, setting up automatic transfers, understanding how compounding works—adds to a sense of control and capability.

One of the most empowering moments was when I made my first contribution to an index fund. It wasn’t a large amount, but it represented a shift in mindset. I was no longer just paying bills—I was actively building something. That small step led to others: increasing contributions, learning more about tax-advantaged accounts, and eventually refinancing to improve my financial position. Each decision, no matter how small, reinforced the belief that I was capable of managing my money wisely.

These small wins create momentum. When you see your investment accounts grow, even slowly, it becomes easier to keep going. Celebrating milestones—like reaching $1,000 in savings or paying off a portion of the mortgage—helps maintain motivation. The goal isn’t to compare yourself to others, but to recognize your own progress. Financial confidence isn’t about having all the answers; it’s about trusting the process and knowing that consistent effort leads to results.

By combining mortgage responsibility with smart investing, beginners can transform fear into empowerment. The home is no longer just a debt—it becomes part of a larger strategy for security and growth. Over time, this integrated approach lays the foundation for lasting wealth. It’s not about getting rich quickly, but about building a stable, resilient financial life, one thoughtful decision at a time. And that’s a journey worth taking.