Why Health Insurance Is the Smartest Part of My Asset Plan

What if the key to protecting your wealth isn’t just about investments—but about what you’re protecting them *from*? I used to think asset diversification meant splitting money across stocks, real estate, and savings. Then a medical emergency changed everything. Suddenly, I saw how one overlooked insurance gap could wipe out years of financial progress. That’s when I realized: health insurance isn’t just a safety net—it’s a strategic asset. Here’s how I reshaped my entire financial plan around it.

The Wake-Up Call: When Health Shook My Financial Confidence

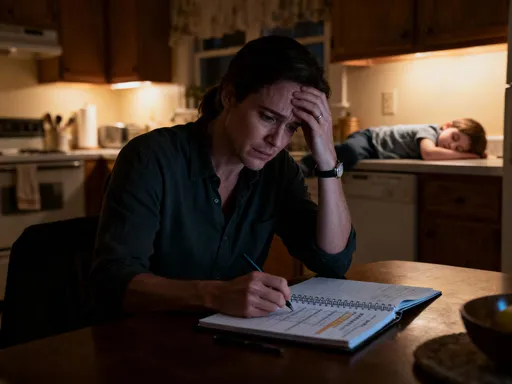

In the spring of 2019, a routine checkup turned into a diagnosis no one expects: a serious but treatable condition requiring surgery and months of recovery. At first, the focus was on healing. But as the weeks passed, the financial reality began to sink in. Out-of-pocket costs for specialists, imaging, medications, and follow-up visits quickly climbed into the tens of thousands, even with insurance. The real shock came when I reviewed my policy and realized it didn’t fully cover rehabilitation services, which were essential for regaining full function. What should have been a recovery period became a financial crisis in slow motion.

This experience shattered the illusion that a strong investment portfolio was enough. I had diversified across index funds, held a rental property, and maintained an emergency fund. Yet none of those assets could absorb the sudden drain of medical debt. I began to question the foundation of my financial planning. Why had I spent years optimizing returns while leaving such a critical vulnerability unaddressed? The answer was discomfort. Talking about illness, especially when feeling healthy, feels like inviting misfortune. But avoiding the conversation didn’t eliminate the risk—it only delayed the reckoning.

What I learned is that financial confidence isn’t just about how much you earn or save. It’s about resilience—the ability to withstand unexpected shocks without derailing long-term goals. A single health crisis can erase decades of disciplined saving, not because of poor investment choices, but because of inadequate protection. This realization marked a turning point: I began to see health insurance not as a monthly expense, but as a foundational layer of financial defense. Without it, even the most carefully constructed wealth plan remains fragile.

Rethinking Assets: Why Protection Belongs in Your Portfolio

Traditionally, financial advisors define assets as things that generate income or appreciate in value—stocks, bonds, real estate, or retirement accounts. Insurance, by contrast, doesn’t produce returns. You pay premiums for years and hope never to use them. On the surface, this makes health insurance seem like a cost rather than an asset. But this narrow view misses a deeper truth: protection itself has economic value. Just as a strong foundation supports a tall building, health insurance supports the entire structure of your financial life.

Consider this: a well-protected individual can afford to take calculated risks in their investments. Knowing that medical costs won’t force the liquidation of assets during a market downturn allows for a more aggressive and potentially rewarding portfolio strategy. In this way, health insurance functions as a form of financial leverage—not by increasing returns directly, but by enabling the conditions under which growth can safely occur. It removes a major source of uncertainty, which in turn increases confidence in long-term planning.

Think of it as risk-adjusted wealth. Two people may have the same net worth on paper, but the one with comprehensive health coverage holds a more stable, resilient version of that wealth. The other is exposed to potential losses that could drastically alter their financial trajectory. By including protection in the definition of assets, we shift from a passive accumulation mindset to an active preservation strategy. This doesn’t mean reducing investment activity—it means strengthening the framework that makes sustained growth possible.

Moreover, the value of health insurance extends beyond immediate cost coverage. It protects earning potential. For many families, the primary income generator is human capital—the ability to work and earn over time. A serious illness can interrupt or even end that stream. Health insurance helps maintain continuity by ensuring access to timely care, minimizing downtime, and supporting a faster return to productivity. In this sense, it’s not just safeguarding savings; it’s protecting future income, which is often the largest component of a household’s financial picture.

The Hidden Cost of Underinsurance: What Most People Miss

Many people assume that having health insurance means they’re protected. But the reality is more nuanced. Standard plans often come with limitations that only become apparent when they’re needed most. For example, a policy might cover hospitalization but exclude certain specialists or advanced treatments. It might have high deductibles, co-pays, or annual caps on specific services. These gaps can lead to significant out-of-pocket expenses, especially for chronic or complex conditions.

Consider a scenario where a woman in her early 50s is diagnosed with a condition requiring specialized care not available locally. She must travel monthly for treatment, incurring costs for transportation, lodging, and meals—none of which are covered by insurance. On top of that, she reduces her work hours, leading to lost income. Over time, these indirect costs accumulate, quietly eroding her savings. Her investment portfolio may look healthy on paper, but the hidden financial drain from underinsurance undermines its stability.

Another common gap is in post-treatment recovery. Physical therapy, mental health support, and home care services are often only partially covered, if at all. Yet these services are critical to full recovery and long-term independence. Without them, the risk of rehospitalization increases, leading to additional medical bills and further income disruption. The financial impact isn’t always immediate, but it compounds over time, especially for families with limited liquidity.

Underinsurance also affects decision-making under stress. When faced with high out-of-pocket costs, patients may delay or skip necessary treatments, opting for cheaper alternatives that could worsen outcomes. This not only harms health but leads to higher costs down the line. The result is a cycle where financial constraints amplify medical risks, and medical issues deepen financial strain. Recognizing these hidden costs is the first step toward building a more complete protection strategy—one that accounts for both direct and indirect expenses associated with health events.

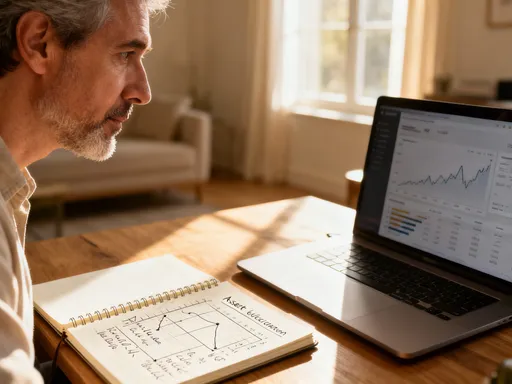

Building a Dual Strategy: Growth + Guardrails

True financial strength comes from balancing two priorities: growing wealth and protecting it. Many people focus intensely on the first while treating the second as an afterthought. But sustainable success requires both. A dual strategy integrates aggressive asset diversification with comprehensive health protection, ensuring that progress isn’t undone by unforeseen events.

Allocating resources to high-quality health insurance isn’t a diversion from wealth-building—it’s an enabler. When you know that medical costs won’t jeopardize your financial stability, you can invest with greater confidence. You’re less likely to panic during market volatility or sell assets at a loss to cover bills. This mental clarity is invaluable. Financial stress impairs judgment, leading to poor decisions. A strong insurance foundation reduces that stress, freeing up cognitive and emotional bandwidth for smarter long-term planning.

Different life stages call for different types of coverage, but the principle remains the same: align protection with financial goals. For example, a young professional just starting out may prioritize affordable coverage with broad access to preventive care. A parent with dependents might focus on plans that include maternity, pediatric, and mental health services. Someone approaching retirement may seek policies that cover chronic disease management and long-term care support. The key is to view insurance not as a static purchase, but as a dynamic component of an evolving financial plan.

It’s also important to consider how insurance interacts with other financial tools. Health Savings Accounts (HSAs), for instance, offer a triple tax advantage: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. When paired with a high-deductible health plan, an HSA becomes a powerful tool for both immediate medical needs and long-term savings. Funds can be invested and grown over time, then used in retirement to cover healthcare costs—effectively turning medical expenses into a tax-efficient withdrawal strategy.

Practical Steps: Aligning Insurance with Life Stages

Financial needs change over time, and so should your health protection strategy. Regularly reviewing and adjusting your insurance coverage ensures it continues to support your overall financial resilience. The goal is not to find the cheapest plan, but the one that best aligns with your current risks, assets, and responsibilities.

For individuals in the early career stage, the focus should be on accessibility and preventive care. This is often a time of lower income but high mobility, so plans with broad provider networks and low out-of-pocket costs for routine visits make sense. Building a habit of regular checkups can prevent more serious (and expensive) issues later. Even at this stage, it’s wise to consider future needs—such as starting an HSA while eligible, allowing decades of tax-advantaged growth.

As family responsibilities grow, insurance needs become more complex. Parents must ensure coverage includes pediatric care, vaccinations, and emergency services. Maternity benefits are essential for those planning to expand their families. At this stage, income protection becomes more critical—disability insurance, often overlooked, can provide a vital safety net if illness prevents work. The financial impact of lost income on a household with children can be devastating, making this an important complement to health coverage.

In the pre-retirement years, the focus shifts toward managing chronic conditions and preparing for long-term care. Medicare becomes a key consideration, but it’s not comprehensive. Many retirees underestimate the out-of-pocket costs for prescription drugs, vision, dental, and hearing care. Supplemental plans or Medigap policies can help fill these gaps. Additionally, long-term care insurance, though often delayed, can prevent the depletion of retirement savings in the event of extended nursing home or in-home care needs. Planning for these expenses in advance allows for more controlled, strategic funding rather than reactive, last-minute decisions.

The most effective approach is to treat insurance reviews as part of annual financial planning—just like checking investment performance or adjusting retirement contributions. Life changes such as marriage, birth, job transitions, or major purchases are natural triggers for reassessment. By integrating insurance into the broader financial conversation, it moves from a peripheral concern to a central pillar of security.

The Psychology of Risk: Why We Ignore What We Hope Won’t Happen

One of the biggest obstacles to adequate health protection is human psychology. We tend to underestimate the likelihood of negative events, especially when they feel distant or abstract. This is known as optimism bias—the belief that bad things happen to other people, not to us. It’s why so many delay buying insurance, skip policy reviews, or choose minimal coverage. The thought of serious illness feels uncomfortable, so we avoid it, often rationalizing that “we’ll deal with it if it happens.”

But this mindset creates a dangerous blind spot. Risk isn’t eliminated by denial; it’s merely deferred. And when a health crisis does occur, the financial consequences are magnified by lack of preparation. Studies show that medical expenses are a leading cause of bankruptcy in many countries, even among those with insurance. The common thread isn’t recklessness—it’s procrastination. People intend to act but never get around to it, until it’s too late.

Overcoming this requires a shift in perspective. Instead of viewing health insurance as a bet against illness, think of it as a form of financial hygiene—like brushing your teeth or changing your car’s oil. It’s a routine maintenance task that prevents larger problems. Just as you wouldn’t skip retirement savings because you’re not yet old, you shouldn’t postpone insurance planning because you’re not yet sick.

Another helpful reframing is to compare insurance to other forms of protection we accept without question. Homeowners insurance doesn’t prevent fires, but we pay for it because we recognize the potential cost of not having it. Similarly, we buy car insurance not because we plan to crash, but because the financial risk of not being covered is too great. Health insurance should be treated with the same seriousness. It’s not about fear—it’s about responsibility. By adopting this mindset, we move from reactive avoidance to proactive stewardship of our financial well-being.

Putting It All Together: A Smarter Definition of Financial Success

Financial success is often measured by numbers: net worth, investment returns, savings rate. But these metrics tell only part of the story. True financial health includes the ability to withstand adversity without losing ground. It’s not just about how much you accumulate, but how well you preserve it. And preservation begins with protection.

Integrating health insurance into your asset plan isn’t about pessimism—it’s about realism. It acknowledges that life is unpredictable and that the best financial strategies are those built to endure shocks. When health coverage is treated as a core component of wealth management, it transforms from a cost center into a strategic advantage. It enables bolder investments, reduces stress, and supports long-term stability.

A holistic financial plan balances growth and guardrails. It recognizes that assets are not just what you own, but what you can keep. In this framework, health insurance is not an optional add-on—it’s a cornerstone. It protects not only your body but your life’s work. By giving it the attention it deserves, you build a foundation that supports every other financial goal, from homeownership to retirement to leaving a legacy.

The smartest part of any asset plan isn’t the highest-return investment. It’s the one that ensures all other investments have a chance to grow. And that, more than anything, is the mark of true financial wisdom.